Phát hiện bài viếtKhám phá nội dung hấp dẫn và quan điểm đa dạng trên trang Khám phá của chúng tôi. Khám phá những ý tưởng mới và tham gia vào các cuộc trò chuyện có ý nghĩa

North America Enterprise WLAN Market Overview: Scope, Value & Key Insights

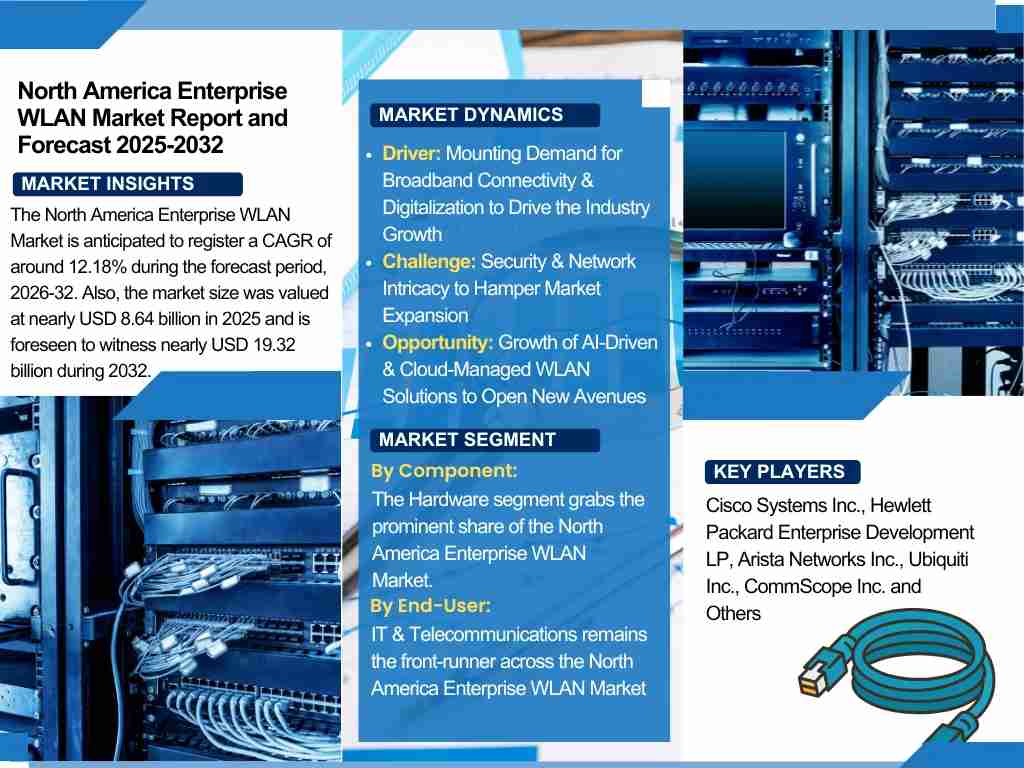

The North America Enterprise WLAN Market is anticipated to register a CAGR of around 12.18% during the forecast period, 2026-32. Also, the market size was valued at nearly USD 8.64 billion in 2025 and is foreseen to witness nearly USD 19.32 billion during 2032. The market expansion is strengthened by surging business development, increasing demand for broadband connectivity, and increasing embracing of market solutions across numerous sectors.

https://www.thereportcubes.com..../report-store/north-

Giống

Bình luận

Đăng lại

South Africa Medical Devices Market Overview: Scope, Value & Key Insights

The South Africa Medical Devices Market reached a value of nearly USD 1.12 Billion in 2025. The market is assessed to grow at a CAGR of around 6.88%, during the forecast period of 2026-2032 to attain a value of around USD 1.67 Billion in 2032. The industry development is driven by the rising healthcare requirements, increasing chronic illnesses, and mounting demand for cost-effective solutions nationwide.

https://www.thereportcubes.com..../report-store/south-

Giống

Bình luận

Đăng lại

Showing 18 out of 499